Updated 8:42 AM ET — NVDA +6.8% pre-market | $238.14

The free cash flow number stopped me cold.

Not the revenue. Not the guidance. Not even Jensen Huang’s closing line about “the largest infrastructure expansion in human history” — which, at this point, lands with the same gravitational weight as a weather forecast. What stopped me was the $48.6 billion in free cash flow that Nvidia generated in a single quarter. Three months. One quarter. For context: that figure exceeds ExxonMobil’s annual profit. It exceeds the combined full-year revenue of Goldman Sachs and Morgan Stanley. It came from a company that, eleven years ago, was primarily known for making graphics cards for people who played video games too seriously.

Nvidia reported Wednesday evening. Revenue of $81.62 billion, up 85% from a year ago. Net income of $58.3 billion, up 211%. Q2 guidance of $91 billion, roughly $7 billion above what the Street had penciled in. The stock dipped 1.5% in after-hours trading on results that would constitute a once-in-a-generation quarter for virtually any other company on earth.

That dip is the story. Not the numbers.

What the Financials Actually Show

The data center segment — $75.2 billion in revenue, up 92% year over year — now constitutes 92% of Nvidia’s total business. Gaming, networking for non-AI purposes, automotive: the rest of the income statement reads like a footnote somebody forgot to delete.

Gross margin came in at 75%, recovering from the 60.8% posted a year ago when a $4.5 billion inventory charge tied to China export restrictions temporarily cratered the profitability picture. Operating profit hit $53.5 billion, up 147%. The company returned $20 billion to shareholders in Q1 alone through buybacks and dividends, then authorized another $80 billion in repurchases and raised its quarterly dividend from one cent to twenty-five cents — a 25-fold increase that got approximately one-tenth the press coverage it deserved.

One number that didn’t make many headlines: operating expenses grew faster than revenue in certain line items. The Rubin architecture launch — Nvidia’s next-generation platform targeting second-half 2026 — is already showing up in the cost structure before it has contributed a dollar of revenue.

| Metric | Q1 FY2026 | Q1 FY2027 | Change |

|---|---|---|---|

| Total Revenue | $44.06B | $81.62B | +85.2% |

| Data Center Revenue | $39.1B | $75.2B | +92.3% |

| Gross Profit | $26.7B | $61.2B | +129.3% |

| Operating Profit | $21.6B | $53.5B | +147.4% |

| Net Income | $18.8B | $58.3B | +210.6% |

| Non-GAAP EPS | $0.78 | $1.87 | +139.7% |

| Gross Margin | 60.8% | 75.0% | +14.2pp |

| Free Cash Flow | — | $48.6B | Record |

| Q2 Guidance | — | $91.0B ±2% | vs. est. $86.84B |

Sources: Nvidia investor relations, CNBC, Quiver Quantitative, LSEG. May 20, 2026.

The Number on Page 22

There is a section of Nvidia’s quarterly 10-Q that gets approximately zero coverage during earnings season. It is not the revenue table. It is not the segment breakdown. It is the customer concentration disclosure, buried in the risk factors on page 22, which has now read as follows for three consecutive quarters:

Four direct customers each accounted for more than 10% of total revenue. Their contributions: 22%, 15%, 13%, 11%.

Combined: 61% of $57 billion in Q3 FY2026 quarterly revenue from four unnamed buyers. For context, one year earlier, three customers accounted for 36% of a smaller base. For the full fiscal year 2026, just two customers accounted for 36% of total annual revenue.

The concentration is getting worse, not better, as the company scales.

I spent some time last week talking to a portfolio manager at a mid-sized fund in Chicago — someone who has owned Nvidia since 2020 and has no particular interest in selling — and even he flagged the customer concentration as the number that keeps him up more than the valuation does. “If two of those four names decide to pause for a quarter,” he said, “there’s nothing in the model that absorbs it cleanly.”

He’s right. There isn’t.

This isn’t a hypothetical tail risk. Nvidia itself acknowledged the trend in its filings, stating: “We have experienced periods where our revenue was concentrated with a limited number of customers, and this trend may continue.” The company is essentially disclosing in its own SEC documents that the risk it most needs investors to overlook is the one that has been quietly intensifying.

China: The $50 Billion Room Nobody Talks About

China represented approximately 13% of Nvidia’s revenue in fiscal 2025, or about $17.1 billion, before U.S. export restrictions cut off advanced AI chip shipments. Nvidia took a $4.5 billion inventory charge on H20 chips that couldn’t be delivered. Another $8 billion in expected H20 revenue evaporated the following quarter. The China AI accelerator market is now projected to reach nearly $50 billion.

That $50 billion market is currently booked as zero in Nvidia’s guidance. The Q2 forecast of $91 billion explicitly excludes any data center revenue from China.

Jensen Huang flew to Beijing with the U.S. trade delegation earlier this month. There are signals that partial restrictions on lower-specification chips may ease. The bull case on China says this is a reopening story in slow motion, and that any reentry — even partial — adds a revenue line that doesn’t currently exist in any model.

Maybe. But CFO Colette Kress confirmed on Wednesday’s call that Nvidia still sees no revenue from the region. And even in the most optimistic scenario, export-compliant chips for China carry meaningfully lower margins than Nvidia’s unrestricted flagship products. The geometry of the upside is narrower than the headline opportunity suggests.

The longer concern is one that Huang himself has articulated, somewhat unusually for a CEO discussing a market he can’t currently access. He has argued that the real risk isn’t losing chip sales — it’s losing the platform. When Chinese developers build workflows on Huawei’s Ascend ecosystem rather than CUDA, they create an alternative stack that doesn’t need Nvidia to function, and that can be exported to other markets. “The AI race is not just about chips,” Huang has said. “It’s about which stack the world runs on.”

He’s describing a platform war. Platform wars, once decided in a major market, have a poor track record of reversing. Nobody went back to Symbian after the iPhone.

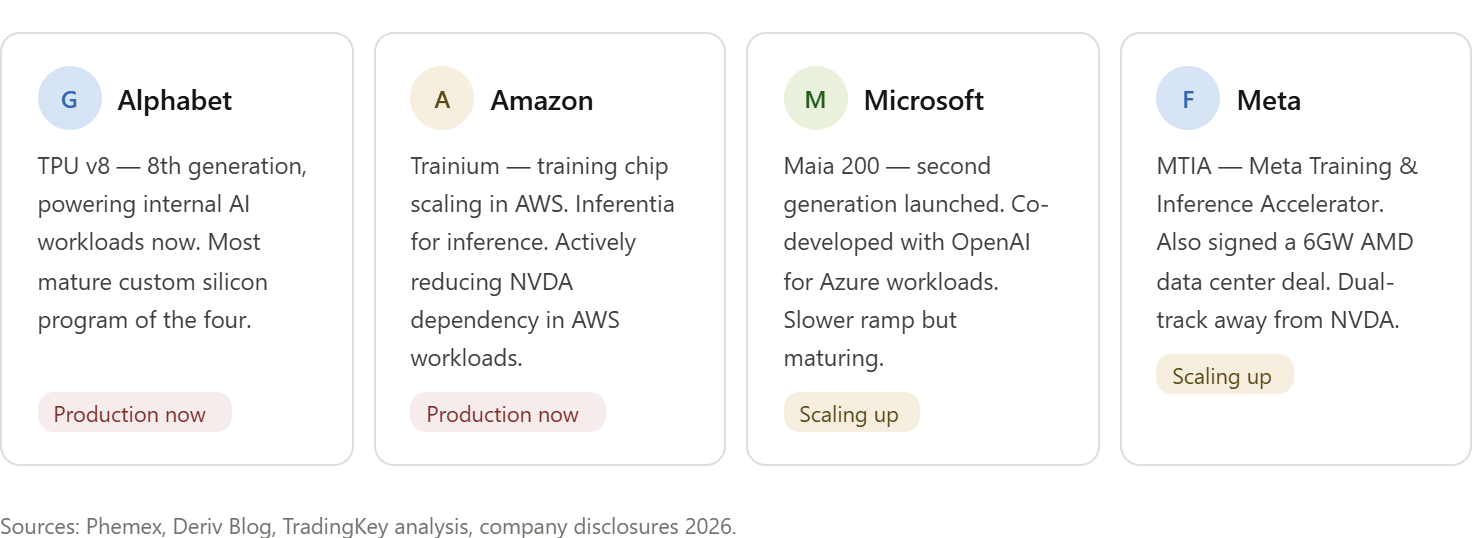

Everyone’s Building Their Own Chips. Slowly. Which Is the Point.

Google is on its eighth-generation TPU. Amazon runs Trainium for training and Inferentia for inference inside AWS. Microsoft launched its second-generation Maia 200. Meta is developing MTIA while simultaneously signing large data center contracts with AMD.

The standard bull response is that none of these chips compete with Blackwell for frontier model training, which is true. CUDA’s software moat — fifteen years deep, embedded in every major research workflow, the lingua franca of AI development — is more durable than the hardware itself.

But the threat doesn’t need to displace Nvidia in training. It needs to capture a meaningful share of inference workloads — the running of already-trained models at scale — where CUDA’s advantages are thinner and where the volume is going as the industry matures. Nvidia spent approximately $20 billion acquiring Groq’s assets in late 2025, specifically targeting the inference market. That acquisition was smart. It was also a signal: management knows where the vulnerability is.

The timeline on custom silicon erosion is three to five years, not three to five quarters. But at $5.7 trillion in market cap, Nvidia is being valued on what happens in three to five years.

What the Analysts Are Saying (and What They’re Not)

| Firm | Rating | Target | Note |

|---|---|---|---|

| Cantor Fitzgerald | Overweight | $300 | Blackwell + Rubin pipeline |

| Bank of America | Buy | $275–320 | FY29 rev. est. $496B |

| Wedbush | Outperform | $275 | AI infrastructure supercycle |

| Goldman Sachs | Buy | $250 | Data center thesis |

| Morgan Stanley | Overweight | $250 | Software ecosystem |

| S&P Global Consensus | Strong Buy | $275.83 | Avg. 61 analysts |

| Alpha Spread (DCF) | — | ~$175 | Fundamental fair value |

| Street Low | Cautious | $140 | Spending slowdown scenario |

Sources: TipRanks, S&P Global, Alpha Spread, analyst research as of May 21, 2026.

Sixty-one analysts. One cautious rating. That kind of consensus is either a sign of exceptional business quality or a sign that the career risk of being wrong in the bearish direction has made the bearish direction professionally unattractive. Probably some of both.

What the consensus targets don’t fully account for is the expectation embedded in the price itself. Bloomberg consensus has already set FY2027 full-year revenue at approximately $370 billion or above — requiring Nvidia to sustain roughly 70% year-over-year growth every quarter with essentially no margin for error. Nvidia’s stock fell 5.5% on earnings day in February 2026 and dropped 3.2% the day after the November 2025 report. Both times the company had beaten revenue estimates. The market has repriced “beat consensus” as the minimum threshold for staying flat. Delivering what you said you would deliver no longer moves the stock.

That’s a difficult dynamic to own into.

The ROI Question, Still Unanswered

Over half of the 4,454 CEOs surveyed by PwC reported no revenue or cost gains from AI yet. Only 8.6% of enterprises report AI agents deployed in production. MIT research from August 2025 found 95% of organizations getting zero return on generative AI investments.

The bulls point to Azure AI revenue growth, Google Cloud backlog expansion, AWS AI services uptake — all real, all growing. The counterargument isn’t that AI isn’t working. It’s that the infrastructure investment is running approximately three years ahead of the revenue it’s supposed to generate, and at some point the CFOs in the room ask what the current year’s GPU budget actually produced.

Bridgewater’s co-CIOs flagged this dynamic months ago, noting that companies are forced to keep investing heavily in AI to avoid falling behind even when short-term returns remain uncertain. That’s a self-reinforcing cycle. Self-reinforcing cycles in capital markets history have a mixed track record of ending gracefully.

The question Nvidia investors need to sit with isn’t whether AI is real. It’s whether the current pace of investment is sustainable long enough for Nvidia’s current valuation to be justified by the earnings that eventually result. Those are different questions. Conflating them is expensive.

Where This Leaves the Stock

Alpha Spread’s fundamental analysis puts Nvidia as overvalued by approximately 22% at current prices, using both DCF and multiples. That’s not a fringe view — it’s what a traditional valuation methodology produces when you don’t assume perpetual hypergrowth.

At $238, the consensus target of $275 implies roughly 15% upside if everything goes right. The street-high of $300 requires Rubin to launch cleanly, China to partially reopen at acceptable margins, and hyperscaler capex to either hold or reaccelerate. The street-low of $140 requires several things to break simultaneously.

This desk’s view sits at $170 to $210 by year-end. The specific mechanism: Rubin creates a one-to-two quarter order pause as hyperscalers decide whether to wait for the new architecture rather than commit more capital to Blackwell. That pause arrives into a market that has already priced in perfect execution. The response to even a modest guidance miss on a 45x trailing P/E stock is not gradual. It’s fast.

There’s a version of 2026 where none of this happens. Where Rubin ramps without friction, where the four unnamed customers keep writing checks, where a hyperscaler CFO never says the word “pause” on an earnings call. That version exists. It might even be the most likely version.

It’s also fully priced in. And then some.

StockVane holds no positions in any securities mentioned. All data sourced from Nvidia investor relations, SEC filings, CNBC, S&P Global, Alpha Spread, Quiver Quantitative, and publicly available analyst research as of May 21, 2026. This article is for informational purposes only and does not constitute investment advice.