Why Nvidia Is No Longer Just a Semiconductor Company

There are very few companies in market history that completely redefine investor psychology the way Nvidia has over the last several years. Apple changed consumer technology. Amazon changed e-commerce infrastructure. Tesla changed how retail investors think about growth stocks. But Nvidia did something even more unusual: it transformed semiconductors — historically one of the market’s most cyclical industries — into the center of the global artificial intelligence narrative.

That shift is the reason Nvidia stock stopped behaving like a traditional chip company and started trading more like a strategic AI infrastructure asset tied directly to the future of global computing. At StockVane, we believe this is the single biggest point many investors still misunderstand. The market is no longer valuing Nvidia simply based on gaming GPUs or quarterly hardware demand. Increasingly, institutional investors treat Nvidia as the “infrastructure landlord” of the AI economy.

That distinction matters enormously because infrastructure companies historically maintain pricing power much longer than hype-driven application companies. The average retail investor still looks at Nvidia and asks whether the stock has become too expensive. Institutional capital is asking a different question entirely: what happens if Nvidia becomes permanently embedded into global computing architecture for the next decade?

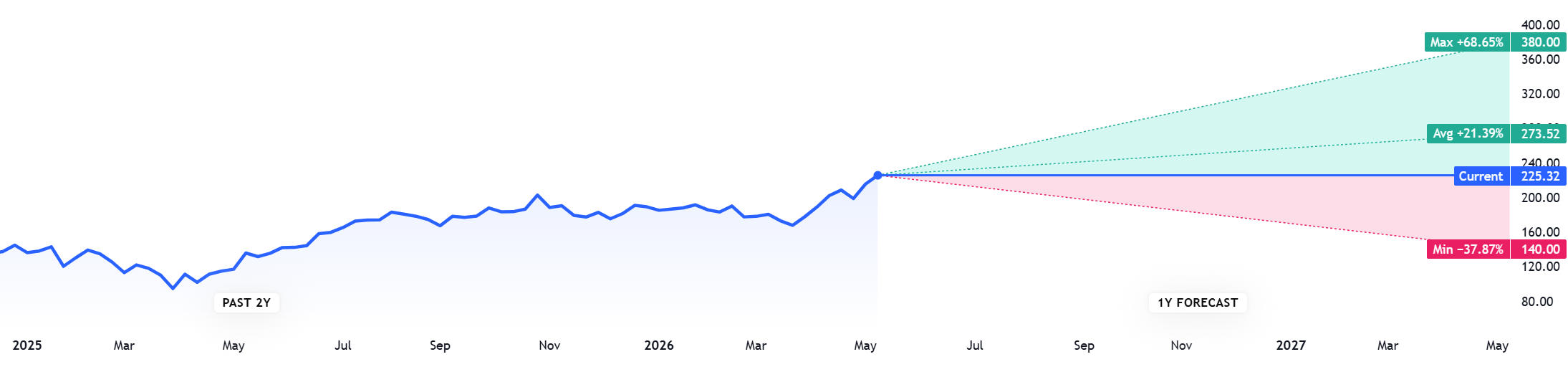

NVDA Stock Price Prediction 2026-2027

Prediction Price from $140 to $380.

This is why Nvidia remains one of the hardest companies to value in 2026. Traditional valuation frameworks struggle to explain a business growing at extraordinary scale while simultaneously generating margins that resemble software firms more than hardware manufacturers. Bears continue arguing that Nvidia’s valuation is unsustainable, while bulls argue the AI revolution has barely begun. Reality is probably more nuanced. Nvidia is neither an unstoppable monopoly nor an irrational bubble. But it may be one of the strongest strategic technology businesses the market has seen in decades.

Nvidia’s Financial Growth Changed the Entire AI Market

The most important thing investors need to understand is how dramatically Nvidia’s revenue model evolved after the AI boom accelerated. Older investors still mentally associate Nvidia with gaming GPUs, crypto mining cycles, and enthusiast PC hardware. That version of Nvidia still exists, but it is no longer the primary engine behind the company’s valuation.

The real story is data centers.

AI infrastructure spending exploded globally after ChatGPT changed public perception of artificial intelligence. Suddenly every major technology company faced the same problem: if AI becomes the next computing platform, nobody wants to fall behind. Microsoft, Amazon, Meta, Alphabet, Oracle, and dozens of sovereign AI initiatives all rushed to secure GPU capacity. Nvidia became the central supplier almost overnight.

The financial numbers behind this transformation remain staggering.

Fiscal 2023 revenue was approximately $26.9 billion. At the time, Nvidia was already considered one of the strongest semiconductor companies in the world. But then the AI infrastructure boom fundamentally changed the scale of the business.

Fiscal 2024 revenue surged to roughly $60.9 billion, driven primarily by hyperscaler AI demand and large language model infrastructure spending. Then growth accelerated even further. Fiscal 2025 revenue exploded above $130 billion according to company-reported results, one of the fastest expansions ever achieved by a mega-cap semiconductor company.

NVIDIA Key Financial Results by Quarter

| Financial Metric | FY2026 Q4(Ended Jan 2026) | FY2026 Q3(Ended Oct 2025) | FY2026 Q2(Ended Jul 2025) | FY2026 Q1(Ended Apr 2025) |

| Revenue | $68.13 B | $57.01 B | $46.74 B | $44.06 B |

| * QoQ Growth | +20% | +22% | +6.1% | +12% |

| * YoY Growth | +73% | +62% | +55% | +69% |

| Gross Margin | 75.0% | 73.4% | 72.4% | 60.5% * |

| Net Income | $42.96 B | $31.91 B | $26.42 B | $18.78 B |

| * YoY Growth | +94% | +65% | +57% | +26% |

| Diluted EPS | $1.76 | $1.30 | $1.08 | $0.76 |

The composition of that growth matters even more than the headline numbers themselves. Nvidia’s data center segment completely overtook gaming revenue as the dominant profit engine. AI accelerators, networking infrastructure, enterprise deployments, and cloud infrastructure spending became the core drivers of valuation.

Revenue Breakdown by Market Segment

This table highlights the transition of hyperscalers and AI clusters entirely onto the Blackwell platform towards late FY2026.

| Segment | Q4 FY26 | Q3 FY26 | Q2 FY26 | Q1 FY26 | Q4 FY25 | Q3 FY25 |

| Data Center | $62.30 | $51.21 | $41.10 | $39.40 | $35.60 | $30.77 |

| * Data Center YoY* | +75% | +66% | +62% | +71% | +109% | +112% |

| Gaming & AI PC | $3.70 | $4.30 | $2.80 | $2.60 | $2.52 | $2.49 |

| Professional Visualization | $1.30 | $0.76 | $0.54 | $0.42 | $0.50 | $0.49 |

| Automotive & Robotics | $0.60 | $0.59 | $0.49 | $0.45 | $0.57 | $0.45 |

| OEM & Other | $0.23 | $0.17 | $0.11 | $0.10 | $0.14 | $0.88 |

Gross margins also tell an important story. Semiconductor businesses traditionally suffer from pricing pressure and cyclical margin compression over time. Nvidia temporarily broke that pattern because AI demand became so urgent that customers prioritized access over price sensitivity. Gross margins climbed into the mid-70% range in several quarters, levels historically associated more with elite software companies than hardware manufacturers.

Financial Soundness & Cash Metrics

| Financial Pillar | Q4 FY26 | Q3 FY26 | Q2 FY26 | Q1 FY26 | Q4 FY25 | Q3 FY25 |

| Cash & Cash Equivalents | $42.10 | $38.40 | $34.80 | $31.20 | $37.72 | $34.79 |

| Operating Cash Flow | $46.20 | $38.80 | $31.50 | $24.10 | $27.50 | $23.90 |

| Free Cash Flow | $43.90 | $36.50 | $29.10 | $22.00 | $25.70 | $22.20 |

| Capital Expenditures (CapEx) | $2.30 | $2.30 | $2.40 | $2.10 | $1.80 | $1.70 |

That profitability is one reason institutional investors became comfortable assigning Nvidia an extraordinary valuation premium.

The Most Important Nvidia Bull Case Nobody Explains Properly

At StockVane, we think many retail investors focus too heavily on GPU demand itself while underestimating Nvidia’s true competitive advantage: ecosystem control.

CUDA may ultimately become more valuable than the hardware.

Developers, AI researchers, enterprises, and cloud providers already built enormous workflows around Nvidia’s software stack. Once organizations optimize infrastructure around Nvidia architecture, switching costs become painful. This dynamic resembles Microsoft’s enterprise dominance during earlier computing eras.

This is why replacing Nvidia is much harder than many headlines imply.

Hardware alone is not enough.

Software ecosystems, deployment reliability, developer familiarity, networking optimization, AI frameworks, and enterprise support all matter. Nvidia built advantages across multiple layers simultaneously, making the company extremely difficult to challenge even as competitors spend aggressively.

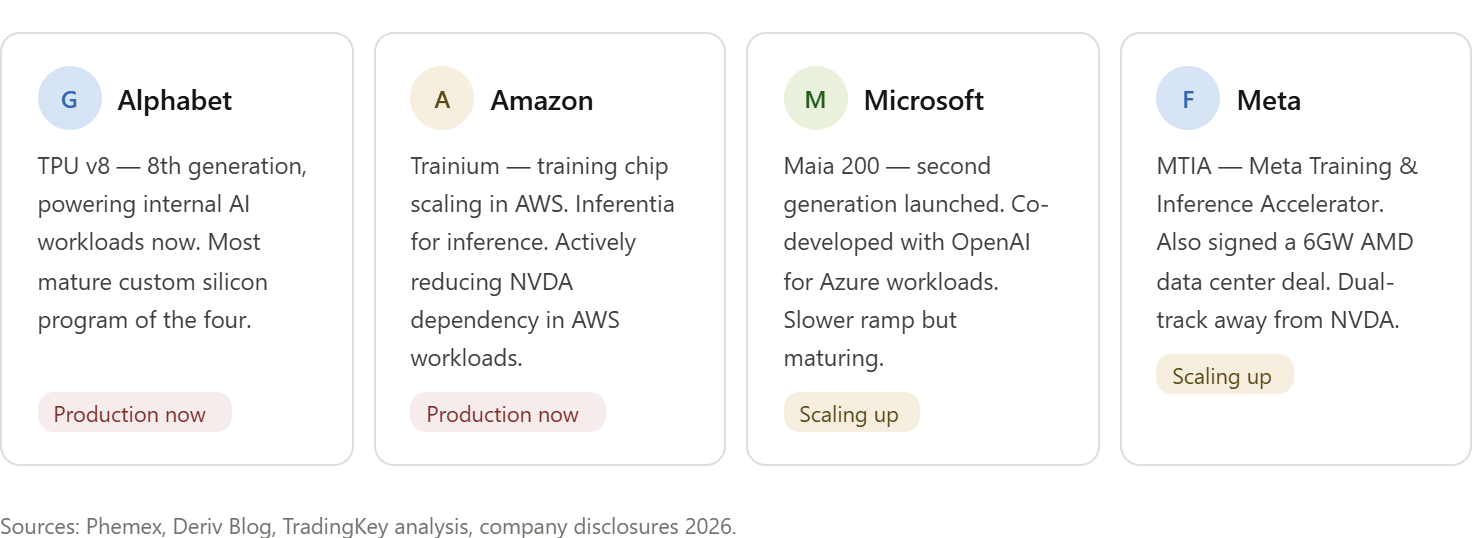

This is also why Nvidia’s biggest long-term threat may not come directly from AMD or Intel, but from its own customers.

Microsoft, Google, Amazon, and Meta all have incentives to reduce long-term dependence on Nvidia by developing custom AI accelerators internally. History shows dominant customers eventually pursue vertical integration whenever supplier power becomes too strong.

Still, replacing Nvidia at scale remains extraordinarily difficult in the near term.

Real Risks Nvidia Investors Need to Take Seriously

One of the biggest mistakes retail investors make is assuming AI infrastructure demand continues growing indefinitely without cycles.

Semiconductor history has never worked that way.

Even dominant chip companies eventually experience digestion periods where:

- customers pause spending

- inventory normalizes

- valuation multiples compress

- infrastructure deployment slows

Right now Nvidia benefits from an almost perfect combination of forces:

- explosive AI demand

- hyperscaler competition

- sovereign AI spending

- limited GPU supply

- retail investor enthusiasm

- institutional momentum buying

It is extremely rare for all these conditions to align simultaneously.

The challenge for investors is determining how sustainable this environment truly is.

At StockVane, we believe AI itself is absolutely real, but investors may still underestimate how cyclical AI infrastructure spending could eventually become. Hyperscalers are spending aggressively because nobody wants to lose the AI race. But eventually shareholders will demand measurable economic returns on those investments.

Questions investors should monitor carefully include:

- How profitable are enterprise AI deployments actually becoming?

- Can hyperscalers maintain current capex growth indefinitely?

- Will AI monetization justify infrastructure spending levels?

- How much pricing power can Nvidia maintain once supply normalizes?

Another overlooked risk involves physical infrastructure constraints. AI data centers require enormous electricity consumption, cooling systems, networking hardware, and manufacturing coordination. In some regions, energy limitations already constrain expansion timelines.

AI growth is not purely digital. Physical infrastructure still matters.

Nvidia Earnings Expectations for 2026

Heading into the next earnings cycle, Wall Street expectations remain extremely high.

Analysts broadly expect continued strength in:

- data center revenue

- Blackwell AI chip demand

- hyperscaler spending

- sovereign AI projects

- enterprise AI adoption

- networking infrastructure growth

Consensus expectations for upcoming quarterly revenue remain in the tens of billions range, with investors focused heavily on whether Blackwell deployment ramps smoothly enough to sustain Nvidia’s current growth trajectory.

However, at this stage the biggest issue is no longer whether Nvidia remains profitable. The market already assumes that.

The real issue is guidance durability.

Investors want confirmation that AI infrastructure demand remains strong well into 2026 rather than peaking during the current spending cycle.

At StockVane, we believe management commentary may matter more than headline revenue numbers themselves. Markets will pay extremely close attention to:

- hyperscaler order visibility

- gross margin sustainability

- enterprise AI adoption trends

- sovereign demand

- supply chain normalization

- customer diversification

Those signals could shape Nvidia’s stock direction more than the raw earnings figures.

Consumer Sentiment and Real User Opinions on Nvidia

One reason Nvidia stock remains psychologically powerful is because consumers genuinely interact with AI products more now than ever before. ChatGPT, AI image generation, autonomous systems, enterprise copilots, recommendation engines, and AI-enhanced cloud tools changed how people perceive computing itself.

Nvidia became the symbolic stock representing that entire transformation.

Consumer sentiment toward Nvidia products remains remarkably strong across gaming communities, AI developer forums, enterprise technology reviews, and investing discussions. Many developers openly prefer Nvidia hardware because of ecosystem maturity and software compatibility. Enterprise users frequently mention deployment reliability advantages. Even gamers who complain about GPU pricing often admit Nvidia still dominates performance perception at the high end.

Representative user opinions commonly seen across forums include:

“Every AI startup pitch deck somehow depends on Nvidia chips somewhere in the stack.”

“I hate how expensive Nvidia GPUs became, but serious AI workflows still run best on Nvidia.”

“The company stopped feeling like a gaming stock years ago. It feels like the backbone of AI infrastructure now.”

“People keep calling Nvidia overvalued, but nobody explains who realistically replaces them over the next three years.”

These comments reflect something deeper than hype. Nvidia increasingly became the public face of the AI era itself.

StockVane’s Nvidia Stock Forecast for 2026

At StockVane, our outlook on Nvidia remains bullish into 2026, but not because we believe hypergrowth continues forever without volatility.

We remain bullish because Nvidia currently occupies one of the strongest strategic bottleneck positions inside the global AI economy.

In many ways, Nvidia resembles a company selling “digital electricity” to the AI revolution. Every major AI model still requires enormous computational infrastructure, and Nvidia continues controlling the most critical layer of that infrastructure stack.

However, investors should absolutely expect:

- higher volatility

- periodic valuation corrections

- slowing growth rates over time

- increasing competitive pressure

- political and geopolitical risks

- customer diversification attempts

The future likely will not look like the straight-line rally investors experienced during the first AI mania phase.

Still, dismissing Nvidia simply because the stock already rose dramatically may remain one of the market’s biggest analytical mistakes.

Some companies become expensive because of hype.

Others become expensive because the market slowly realizes they are more important than previously understood.

Nvidia increasingly looks like the second category.

#NvidiaStock #NVDA #AIStocks #ArtificialIntelligence #StockMarket #TechStocks #Semiconductors #Nasdaq #StockVane #EarningsReport

Pingback: Everyone Is Bullish on Apple Stock Right Now, That’s Exactly Why I’m Not – StockVane

Pingback: AI Infrastructure Stocks 2026: Who Profits From the $700 Billion Spending Wave – StockVane