Back in October 2019, I had $4,200 sitting in a brokerage account doing absolutely nothing, waiting for Boeing to drop to a price I actually liked. It never did. Not that month, not that quarter. Meanwhile, a guy in my old trading Discord kept posting screenshots of premium he was collecting by selling puts on stocks he also wanted to buy but at lower prices, and I remember thinking, somewhat bitterly, that I’d been doing this wrong for years. Cash sitting idle is a choice, and it’s usually the wrong one. That was my entry point into selling puts, and fifteen years of trading later, it’s still one of maybe four strategies I actually use with real money instead of just knowing about theoretically.

I want to walk you through this properly, not the Instagram-reel version where someone screenshots a green P/L and calls it a system. Real numbers, real trade-offs, and the specific ways this goes badly for people who treat it as a cheat code instead of what it actually is.

One thing up front: nothing here is personalized financial advice. I’m telling you how the mechanics work and how I personally think about risk after doing this for a long time. Options obligate you to buy shares even during a crash, and that’s real money at real risk – size accordingly, and talk to a licensed advisor if you’re managing anything beyond play money.

Table of Contents

- The Mechanics, Without the Jargon

- Why This Beats Just Sitting on a Limit Order

- Put Selling vs Buying the Stock Straight Up

- The “90% Expire Worthless” Line Everyone Repeats (And Why It’s Wrong)

- A Trade Walked Through With Real Numbers

- Where This Actually Goes Wrong

- The Wheel: What Happens After You Get Assigned

- Rules I’ve Actually Stuck To, Not Just Written Down

- What This Looks Like With a Real Portfolio Size

- My Honest Take After All These Years

1. The Mechanics, Without the Jargon

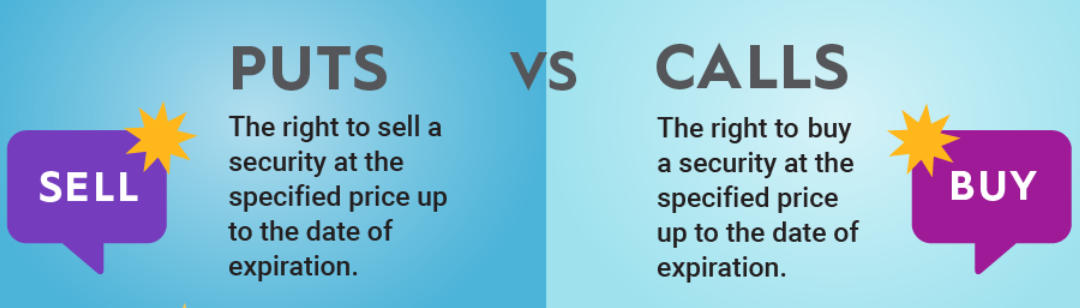

Selling a put is a promise, and it’s worth thinking of it that way instead of as some abstract financial instrument. You’re telling the market: “If this stock falls to $X by this date, I’ll buy 100 shares at $X, no argument.” Someone pays you cash right now for that promise. If the stock never gets there, the promise expires, nothing happens, and you keep the cash. If it does get there, you’re buying shares – that’s assignment, and it’s not a punishment; it’s the deal you signed up for.

A cash-secured put just means the money to actually buy those shares is sitting in your account the whole time, not borrowed. This is the boring, responsible version of the strategy, and it’s the only version I’d suggest anyone reading this actually use.

2. Why This Beats Just Sitting on a Limit Order

Here’s the thing that took me embarrassingly long to internalize. A limit order sitting below market price is a bet that costs you nothing to place and pays you nothing while you wait. It’s passive in the least useful sense of the word – you’re just hoping. Selling a put at that same price level gets you paid for the wait itself. Boeing never hit my price back in 2019, but if I’d sold puts instead of parking a limit order, I’d have collected premium every single month that price target didn’t happen, instead of collecting nothing.

That’s genuinely the whole pitch in one paragraph. Everything else in this article is detail and risk management around that one idea.

3. Put Selling vs Buying the Stock Straight Up

| Factor | Buying Shares Directly | Selling a Cash-Secured Put |

|---|---|---|

| Cash flow on day one | You pay, nothing comes back | Premium lands in your account immediately |

| Real cost basis if things go your way | Whatever the market price was | Strike minus premium – almost always cheaper |

| If the stock rips higher and never dips | You’re along for the whole ride | You keep the premium, miss the ride entirely |

| If the stock falls off a cliff | You eat the full loss on paper | You’re still obligated to buy at strike; premium only softens it a little |

| Capital tied up | Full share price times 100 | Strike price times 100, held as collateral |

Look at that third row for a second, because it’s the part nobody wants to dwell on when they’re excited about the strategy. You give up the moonshot scenario. If the stock does nothing but climb for a year, the stock buyer wins bigger. Put selling is a strategy for people who’d rather trade some upside for a steadier, income-shaped return, not for people chasing the next 300% winner.

4. The “90% Expire Worthless” Line Everyone Repeats (And Why It’s Wrong)

I need to get this off my chest because it’s everywhere in retail trading content, usually attached to some course being sold for $997. The claim is that 90% of options expire worthless; therefore selling options is basically printing money. It’s not true, and the actual Chicago Board Options Exchange numbers tell a more honest story.

| What Actually Happens to an Option Contract | Real CBOE Frequency |

|---|---|

| Closed out before expiration (profit or loss) | 55%-60% |

| Expires worthless, no action taken | 30%-35% |

| Exercised or assigned | Roughly 10% |

The math error people make is treating “only 10% get exercised” as if it means “so the other 90% must expire worthless.” It doesn’t. More than half of all contracts get closed out early, at a gain or a loss, well before anyone gets to the expiration date at all. The real worthless-expiration number is around a third. Still a decent statistic if you’re a seller, genuinely, but it’s not the guaranteed-win narrative the marketing version implies, and I’d trust any writer more who leads with the accurate number instead of the flashy wrong one.

5. A Trade Walked Through With Real Numbers

Let’s use a plausible example instead of vague percentages floating in the air. Stock trading at $150. You’d be genuinely happy owning it at $140 – not “I guess I’d hold it,” but actually happy. You sell a $140 put, 30 days out, and collect $3.50 per share, which is $350 cash landing in your account today for one standard contract.

| What the Stock Does | What Happens to You | Bottom Line |

|---|---|---|

| Stays above $140 | Put expires, no assignment, nothing else happens | Full $350 kept, done |

| Drifts down to $135 | Assigned, you buy 100 shares at $140 | Real cost basis is $136.50, still better than buying outright at $150 originally |

| Crashes to $110 | Still assigned at $140, no way around it | Cost basis $136.50, stock worth $110 – you’re down $26.50 a share on paper, premium or no premium |

That last row is the one nobody screenshots for Twitter. The premium is a cushion, not a parachute. If a $110 print on that stock would genuinely rattle you, the position was too aggressive from the start, full stop, no amount of premium changes that math.

6. Where This Actually Goes Wrong

I’ve watched this happen to people, and honestly did a version of it myself early on. You start selling puts on a stock you don’t actually care about owning, purely because the premium looked fat that week. Then the stock drops, you get assigned, and now you’re holding shares of a company you never wanted in the first place, sitting on a loss, with no real conviction to hold through the recovery. That’s not a put-selling problem specifically – that’s what happens any time you let a number on a screen override your actual judgment about a business.

Elevated volatility is the trap that catches even experienced people. When markets get jumpy – and if you’ve been paying attention to the semiconductor pullback and general risk-off mood lately, you know exactly what I mean – put premiums swell because implied volatility swells with them. A fat premium during a scary week feels like a gift. Sometimes it is. Sometimes the market’s pricing in real risk that’s about to show up in the stock, and you’re the one who just agreed to buy the falling knife at a “discount” that turns out not to be much of one.

7. The Wheel: What Happens After You Get Assigned

Assignment isn’t the end of the strategy, it’s usually the middle of it. Once you own the shares, plenty of people – myself included, most of the time – turn around and sell covered calls against that same stock. Collect more premium, and either get called away at a price you’re happy with, or keep holding and keep collecting. Sell put, get assigned, sell call, repeat. People call this “the wheel,” and it’s popular for a reason: it turns a single trade into an ongoing process instead of a one-time bet.

8. Rules I’ve Actually Stuck To, Not Just Written Down

These aren’t theoretical. These are the specific things that have kept me out of trouble, sometimes because I learned them the expensive way first.

Only sell puts on stocks you’d hold for years if assigned. If the idea of owning it for a while genuinely bothers you, you picked the wrong stock, not the wrong strategy.

Keep the actual cash sitting there. I know someone who sold puts against margin he didn’t actually have covered, got assigned on three positions in the same rough week, and had to liquidate an unrelated position at a bad time just to settle up. Don’t be that guy.

Resist the urge to chase the juiciest premium on the chain. The fattest number is usually fat for a reason, and that reason is rarely in your favor.

Keep position sizes sane relative to your whole portfolio. If getting assigned on one name would suddenly make it 40% of your account, you sized it wrong before you ever placed the trade.

9. What This Looks Like With a Real Portfolio Size

Take someone with $50,000 in cash sitting around, eyeing three or four solid large-cap names they’d happily own 5-8% cheaper than today’s price. Instead of parking limit orders and hoping, they sell cash-secured puts across those names, collecting somewhere in the $800-1,200 range across a 30-45 day cycle, depending on how jumpy the market is at the time.

If nothing dips to the strikes, the premium gets banked and the cycle repeats – a real yield on cash that would otherwise be earning nothing while waiting for an entry point that may or may not ever arrive. If something does get assigned, that person now owns a company they actually wanted, at a genuine discount, with the premium further softening the entry. Neither outcome is a bad one, because both were priced into the decision from the start. That’s the entire trick – picking strikes based on real conviction, not based on which one pays the fattest premium that afternoon.

10. My Honest Take After All These Years

I still think this is one of the more sensible options strategies a retail investor can actually use, mostly because the worst realistic outcome is owning a stock you already decided you wanted, just a little earlier or a little cheaper than you’d planned. That’s a fundamentally gentler risk profile than strategies where the entire premium just vaporizes and you’re left with nothing to show for it.

But I’ve also watched enough people treat this like a magic income button to know where it actually breaks. It breaks when the premium becomes the goal instead of the stock ownership being the goal. It breaks when people oversize because the math looked good on a spreadsheet. It breaks when someone sells puts on a name they’d never otherwise touch, purely chasing yield, and then the stock gaps down 20% overnight on news nobody saw coming, and suddenly they own something they never actually wanted at a price they never actually agreed to in spirit, even if they technically agreed to it on paper.

If you’re going to try this, start small. One contract, on a company you already follow and would genuinely be glad to own more of. Sit through a full cycle before you scale anything up. The strategy rewards patience and real conviction far more than it rewards chasing whichever strike happens to pay the most that week – and that’s really the whole difference between people who use this well for years and people who blow themselves up on it in month three.